Inovio Stock: Adrift At A Bargain Price But No Near-Term Catalyst …

DavidMSchrader/iStock via Getty Images

This is my sixth Inovio (NASDAQ:INO) article, the second since the pandemic following 07/2022’s “Inovio: After All These Years” (“These Years”). In this article I will examine Inovio’s recent Q4, 2022 earnings call (the “Call”) as reported on 03/01/2023. The Call has been disastrous for Inovio’s shares.

I will discuss the why’s and wherefores of the situation.

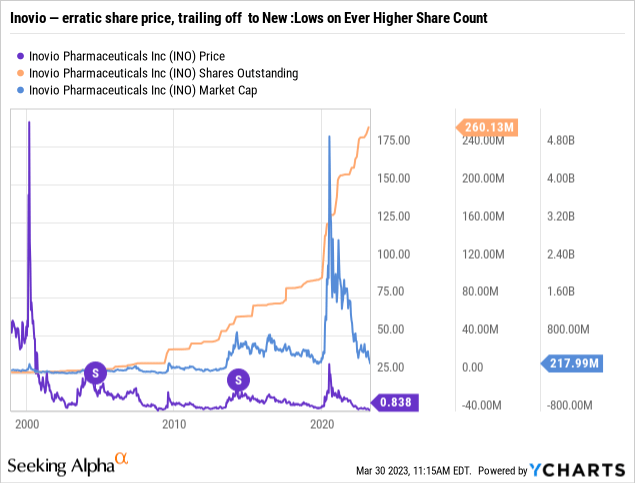

Inovio’s recent share drop below £1.00 is a new and unprecedented development

You have to travel deep into the wayback machine to 02/2009 to find intraday Inovio trading below £1.00. You have to go even further to 11/2008 to find a <£1.00 closing trade. Its previous <£1.00 closing nightmare only lasted ~1 month.

Traveling back in time, it never recurred.

Accordingly, Inovio’s 03/22/2023 <£1.00 close was a real aberration. It is an aberration that has been repeated every subsequent closing up to the date I write on 04/02/2023.

As reflected by the chart below, not only has Inovio steered clear of <£1.00 closings over much of its history, it has traded well above £10.00 for lengthy stretches:

Data by YCharts

Data by YCharts

In 2004 and again in 2014, it goosed its share price and reduced its share count with 1:4 reverse splits. Its stock was not trading near £1.00 a share on either occasion.

This go-around, if its <£1.00 situation persists, it may be headed for a non-optional reverse split to maintain its NASDAQ listing.

If you were an Apple (AAPL) shareholder on 08/31/2020 you likely enjoyed looking at your statement and seeing a 4X factorial increase in your shareholdings. The split didn’t really do anything substantive. It just took your Apple stake and the stakes of all the millions of other Apple shareholders, and sliced them into 4X smaller pieces.

Reverse splits are the mirror opposite.

In a factorial 4 (1:4) reverse stock split everyone’s shares are redistributed into 4X larger chunks. As I explained recently, a reverse split has no impact on shareholders’ proportional ownership in a company. It simply raises the company’s share price and reduces its share count by the selected factorial.

Suppose a company wants to increase its share price by a factor of 4.

It decides on a 1 for 4 (1:4) reverse split. After the reverse split the company’s share price will rise and its count fall by a factor of 4.

If Inovio were to effect a 1:4 reverse split at a time you owned 2,000 shares trading at £0.80, despite your 4X reduced share count, your percentage ownership in the company remains unchanged. The company’s overall share count would be reduced and the price per share increased by the same factor 4.

Your previous stake of 2,000 shares at £0.80 would be recast into 500 shares trading at £3.20.

Whether such a reverse split would materially impact the company’s price over time is unclear. It would likely be received by the market as a sign of weakness, as such its secondary impact would be a drag on the stock.

Several collapsing catalysts are contributing to Inovio’s share weakness

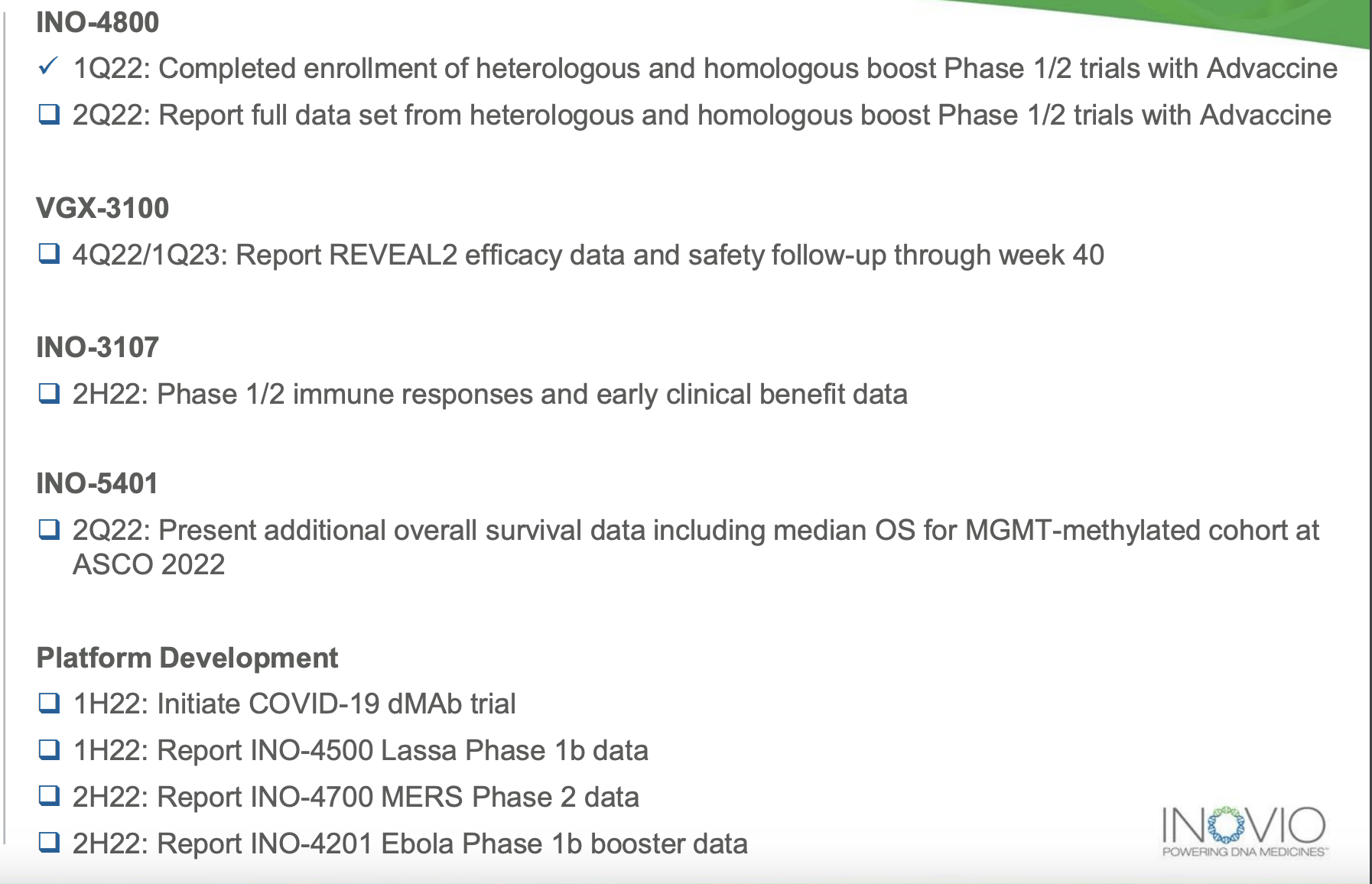

These Years included an Inovio graphic titled “Well-Balanced Pipeline of Milestones”. It included the following listed milestones as of 03/31/2022:

seekingalpha.com

As I write on 03/31/2023 there are several sources of final 2022 Inovio reports:

- the Call;

- Inovio’s Q4, 2022 10-K (the “10-K“) filed on 03/01/2023;

- Inovio’s 03/2023 presentation (the “Presentation“);

- CEO Shea’s 03/13/2023 transcript at the Oppenheimer 33rd Annual Healthcare Conference (“Transcript“).

These sources, particularly Presentation slide 4, provide grist for bringing Inovio’s 03/31/2022 milestones current to the close of 2022.

- INO-4800 — program discontinued, 10-K (p.

10);

- VGX-3100 — (REVEAL2) – Cervical High-Grade Squamous Intraepithelial Lesions (HSIL) o Completed: Announced Phase 3 data (non-registrational study) o Next milestone: Evaluating next steps after analysis of data;

- INO-3107 — Recurrent Respiratory Papillomatosis (RRP) o Completed: Announced positive Phase 1/2 interim data o Next milestone: Initiate Phase 3 (registrational) trial;

- INO-5401 — Glioblastoma (GMB) o Next milestone: Provide update for clinical development plans;

- Platform development — despite being well tolerated Inovio decided to discontinue MERS and Lassa fever candidate development, 10-K (p.

12); its COVID-19 dMAb trial is ongoing; INO-4201 – Ebola o Completed: Announced positive Phase 1 data for INO-4201 as a booster for rVSV-ZEBOV (Ervebo(R)) o Next milestone: Submit data for publication in peer-reviewed journal and determine next steps with partners.

Tallying up, Inovio scores poorly for 2022. Yet dropping programs that are not performing is a net positive step for a little development stage biotech like Inovio. It has limited resources which will be fully utilized in analyzing its next steps.

INO-3107 is leapfrogging VGX-3100 as Inovio’s lead therapy

VGX-3100 has been a particularly difficult asset to develop.

Inovio acquired it as a phase 1 asset back in 2009 when it merged with VGX Pharmaceuticals. Back in 2017 when I wrote my first Inovio article, it was Inovio’s lead asset in phase 3 development.

It encountered a brief clinical hold in 2016 which was lifted in 2017. It was only able to meet its primary endpoint in REVEAL-1 by rejiggering the evaluated population.

It is having a worse time with REVEAL-2. As stated in the 10-K (p.

55):

In March 2023, we announced data from our REVEAL2 trial. Statistical significance was not achieved in the investigational biomarker-selected population for the endpoint of lesion regression and viral clearance.

However, statistical significance was achieved in the all-participants population for the endpoint of lesion regression and viral clearance.

In line with FDA suggestion it is being considered as an exploratory, non-pivotal, trial with one or two more “well-controlled trials” required. That change would then leave Inovio devoid of pivotal trials.

In Presentation slide 4 it points to its planned trial in INO-3107 – Recurrent Respiratory Papillomatosis (RRP) as registrational. in the Transcript, CEO Shea characterizes RRP as an awful disease . It is a virus causing wart-like growths in the respiratory system.

They interfere with talking and in children with breathing.

The only current treatment is surgery. Surgery doesn’t clear the virus so they often regrow. In some patients requiring multiple surgeries in a year.

In response to Transcript interviewer concern that surgery is a problematic endpoint, CEO Shea described Inovio’s experience with its 32 patient phase 1/2 trial.

She characterized the trial as one to evaluate INO-3107’s ability to lessen a patient’s burden of surgeries in patients who had had two or more surgeries the previous year. Patients were given four doses of INO-3107 and followed for 12 months to see what their requirement for surgeries would be. The data showed:

…we saw 81%, or 26 out of 32 showed a reduction in surgeries compared to the prior year.

Inovio is hoping that this data coupled with a favorable safety and tolerability profile will convince the FDA to authorize the design of a registrational phase 3 study.

Inovio’s liquidity should cover its operations over the next year

Inovio’s presentation slide 3 advises that its EOY 2022 liquidity of £253.0 million is expected to fund company operations into Q1, 2025.

CFO Kies describes Inovio’s forward financial situation as follows:

…our projected cash runway into first quarter 2025 includes a cash burn estimate of approximately £32 million for the first quarter of 2023. These projections do not include any funds that may be raised through our existing at-the-market program or other capital-raising activities. …

Its 10-K lists the following as its annual operating losses for years 2020-2022:

![]()

seekingalpha.com

Its 2022 operating loss of ~£267 million would more than eat up its £253 million of liquidity. Similarly its net cash used in operations for 2022 of £216.2 million (10-K p.

60) seems at odds with its anticipated cash runway.

During the Call CFO Kies advised that its Q1, 2023 cash burn estimate was £32 million. Projected at the same rate over the ensuing seven quarters would see it burning cash through 12/31/2024 of £256 million, not quite getting it to year 2025.

Conclusion

Inovio is on the sale of its lifetime as I have noted. It appears to have ample near term liquidity absent some unexpected cataclysm.

Yet ought one buy at sale? Not me.

There are no apparent strong catalysts to move it either up or down. It is adrift.

Its market cap as I write on 04/02/2022 is ~£215 million, not far from its cash of £265 million, less its Q1, 2023 burn of ~£32 million.

Editor’s Note: This article covers one or more microcap stocks.

Please be aware of the risks associated with these stocks.